Microsoft Azure

Microsoft Azure Cloud Financial Management (FinOps)

Cloud Financial Management (FinOps) How to Operationalize FinOps

How to Operationalize FinOps

Wherever you are on your cloud journey, you’re likely under pressure to cut or at least control your cloud spend. You may be undertaking “quick fix” cost cutting tactics such as turning off resources or moving workloads to cheaper services. But, as you may be finding out, tactical, reactive cost management activities generally only work for the short term and do not solve systemic inefficiencies that only increase over time if not addressed.

Given the scale and complexity of today’s multi-cloud environment, not to mention the interdependence between cloud costs and infrastructure, organizations need to change the way they approach cloud cost management.

At Spot, our mission is to help you gain true efficiencies and business value from your FinOps and cost management practices. We do this by delivering holistic, multi-cloud visibility and deep insights together with AI-driven automated cost and infrastructure optimization and embed these processes directly into your operations and workflows. The Spot solutions for FinOps help you generate both immediate and long-term cost savings, accurately budget and control costs, and continuously optimize cloud infrastructure to maximize efficiency.

A major leap: Delivering FinOps through a unified experience

This past June at the FinOps Foundation’s FinOps X conference, we previewed our roadmap for our new FinOps capabilities, including the plan for integrating CloudCheckr capabilities into the Spot console. Our immediate goal is to give our customers the insights and management they need to support their FinOps journey through a unified experience, powerful visibility and analytics, automation, and enhanced workflows.

We have received a fantastic response and helpful feedback on our plans over the past few months. And now, at AWS re:Invent 2023, we’re delighted to show how we are delivering on our commitment to our customers.

As we transform and build out our FinOps capabilities, we are delivering two integrated products through the Spot console: Cost Intelligence, which delivers granular, actionable analytics on costs and resources across multi-cloud environments, and Billing Engine, which streamlines invoicing and delivers comprehensive billing reporting with intelligent cost allocation including chargeback/showback.

These products are built upon and significantly extend tried and tested CloudCheckr capabilities, as well as incorporate new functionality based on customer, FinOps, and industry requests, requirements, and standards. They are designed to deliver the key FinOps capabilities needed by both enterprise organizations and managed service providers (MSPs), and they enhance the value customers realize when using the entire Spot portfolio for FinOps. Cost Intelligence and Billing Engine are in private preview and are expected to be generally available for enterprises in early 2024 and for MSPs in Q2 2024.

- Learn more about Cost Intelligence

- Learn more about Billing Engine

- Learn more about Spot’s support for the FinOps Foundation FOCUS specification

- Learn how to get early access to Cost Intelligence and Billing Engine

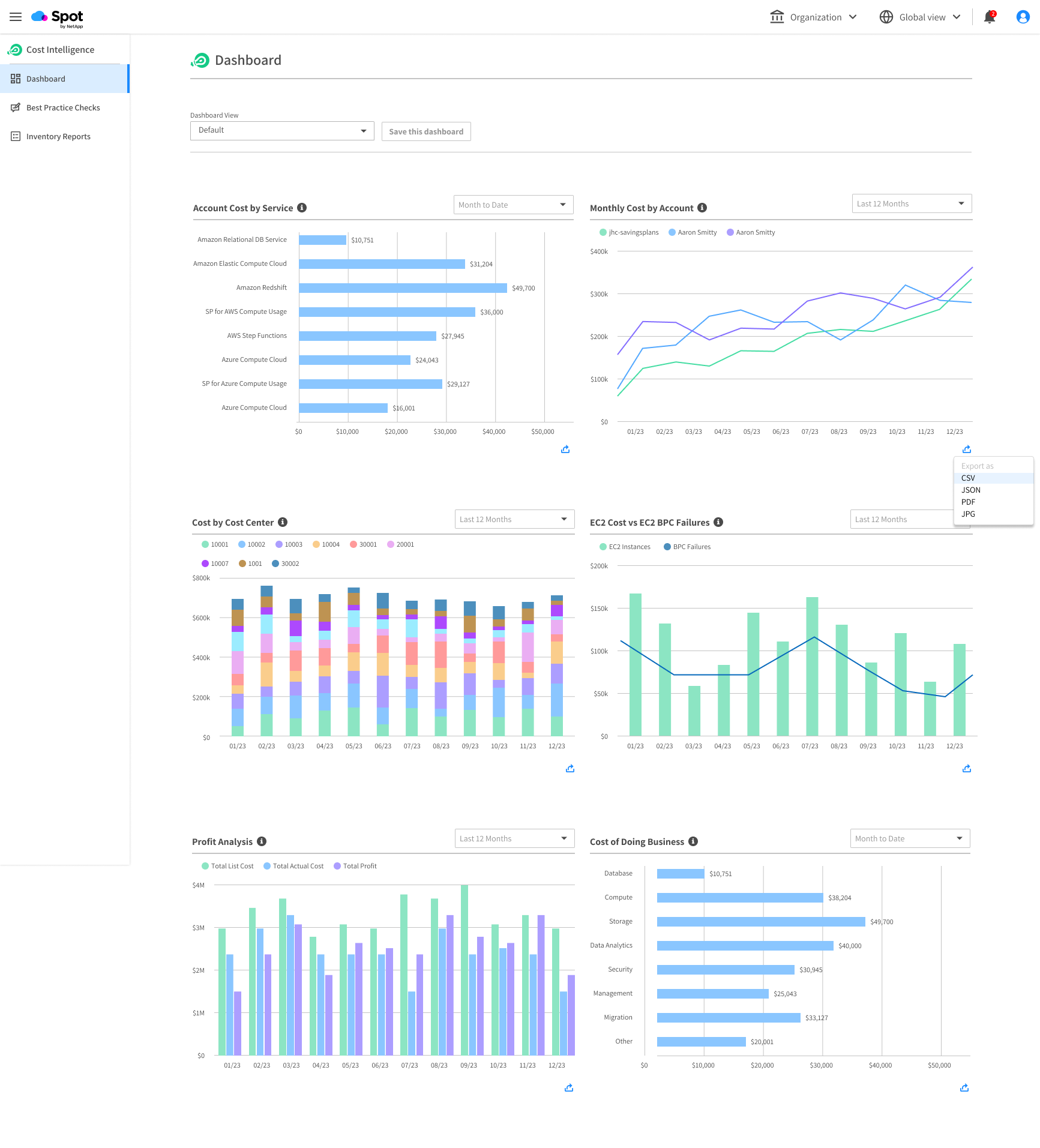

Cost Intelligence: Reduce costs through actionable insights on your cloud environment, all in one place

Organizations and MSPs cannot manage what they cannot see. They must be able to quickly and easily consume and analyze costs across multi-cloud environments and be able to take the right actions to optimize spend. But with sprawling, complex cloud deployments and organizational silos, getting a complete and detailed view of the cloud estate and associated costs is difficult and time consuming, especially if multiple cloud providers are used. It is also challenging to find forgotten or misplaced cloud resources – resources that are driving up costs unnecessarily, not to mention the increasing security risk.

Dynamic customizable visualizations of cloud costs

Cost Intelligence provides deep, actionable analytics on current and historical cloud costs through reports and interactive dashboards that can be customized based on role (Executive, Finance, DevOps, Cloud Manager, Product Owner etc.), FinOps area of interest (cost analysis, resource optimization etc.), or any way you want.

These dashboards and reports can aggregate and display data across accounts and all three primary cloud providers. This gives stakeholders a 360-degree view of their cloud cost performance, helping you understand how and why costs were generated – analysis that goes well beyond what is possible with individual cloud provider native tooling. Cost Intelligence’s dashboards and reports can also include cost customizations that have been applied to billing data to ensure that everyone is viewing and relying on a single source of truth for cloud costs and usage amounts.

A complete inventory of cloud resources and services

Beyond cost analytics, Cost Intelligence also provides detailed cloud inventory reports that deliver at-a-glance, up-to-date snapshots of all the services in your cloud environments (running on AWS, Azure, and Google Cloud) including their properties to help you plan for optimal resource utilization. With Cost Intelligence you no longer need to spend valuable time trying to map your cloud based on piecemeal data in each cloud provider’s console. Through these reports, you will know which cloud services are in use across your cloud estate, how much they cost, and what’s driving those costs.

Actionable insights

With Cost Intelligence’s insights, you can quickly determine where to focus and take the right actions to efficiently and effectively remove waste, right-size instances, prevent cost overruns, optimize cloud costs, and generate operational efficiencies. You can also utilize Spot Eco to build and optimize a smart commitment portfolio, Spot Ocean and Spot Elastigroup to optimize VMs and container infrastructure to efficiently support application workloads, and Spot Security to address cloud misconfigurations, vulnerabilities and other security risks—all from within the Spot console.

Best practice checks to flag deviations in real time

While visibility and insights that drive short- and long-term decisions are critical, a successful FinOps practice also needs the ability to quickly identify and fix unanticipated deviations and outliers in cloud resource usage, configurations, costs, and availability. If not addressed, they will continue to generate waste, rack up costs, and create unnecessary risks. They also become entrenched in your cloud environment, which may be even more dangerous. However, the overwhelming amount of data about cloud costs, resources, and configurations makes detecting, prioritizing, and fixing deviations from the norm a near impossible task. It requires staff with the necessary expertise who can quickly consume all this data – all in real time.

Cost Intelligence’s automated best practice checks (BPCs) do this all for you. Supporting AWS and Azure initially, with Google Cloud in early 2024, Cost Intelligence delivers near-real-time analysis of cloud costs, usage, and performance issues; flags and prioritizes inefficiencies and anomalies; and provides actionable remediation steps to optimize savings and resource utilization and eliminate waste – ready to run out-of-the-box.

With Cost Intelligence’s BPCs, users with any level of experience can immediately and easily understand and respond to critical issues or concerning trends before they get out of hand. Best practice checks are filterable and can be sorted by account. You can also drill down into each type of check to see the impacted resources, their metadata, and all the related infractions in one go.

Access control

Cost Intelligence supports rigid access control requirements to ensure that users/teams only have access to the data that’s applicable to them.

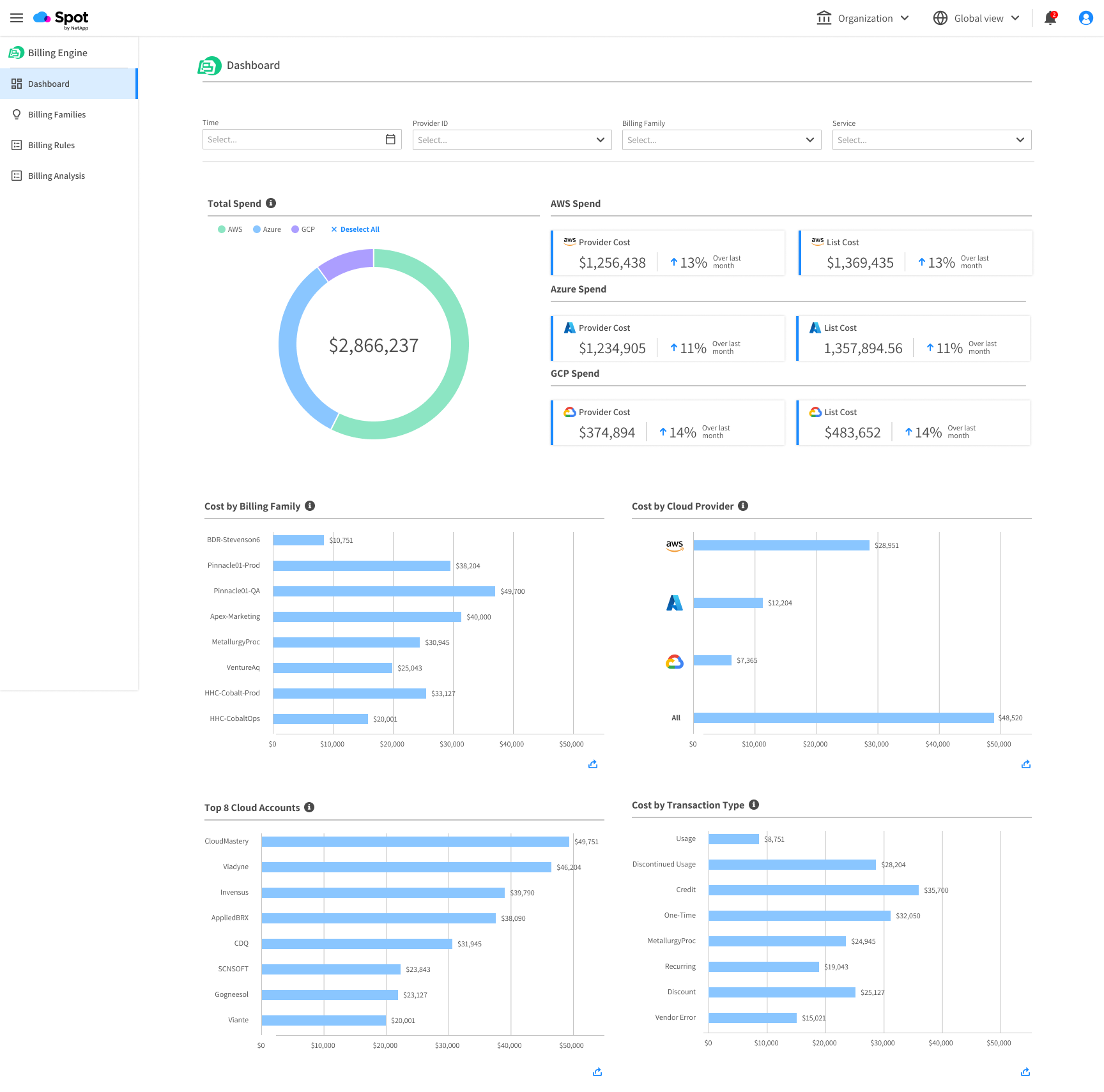

Billing Engine: Control cloud spend granularly and drive accountability across cost centers

Organizations need a way to accurately allocate and bill cloud consumption to the right business unit, product team, customer or any other cost center for cost management, financial accounting, and business purposes. However, the detail and complexity of the cloud provider bills and wide variety of pricing models, tiers, and purchasing packages (which vary from cloud provider to cloud provider), make it extremely difficult to accurately allocate costs and create invoices for chargeback and showback.

To add to the complexity, both enterprises and MSPs need the flexibility to implement specific billing rules, such as distributing or retaining credits and volume-based pricing savings, creating custom charges, and applying discounts or uplifts for shared services. And when an organization has a custom agreement with a cloud provider and/or their customers, these complexities are further compounded. The ability to accurately invoice for cloud is a business-critical issue that directly impacts an organization’s top line revenue and bottom-line profit margins.

Streamlined flexible billing and granular cost allocation

Billing Engine removes the complexity from the invoicing process, accurately managing the nuances of each cloud provider’s costs, and the organization’s cost customization requirements and business agreements. Billing Engine will automatically generate invoices and accurately allocate cloud spend from AWS accounts, Google projects, or Azure subscriptions to the right cost center for chargeback/showback, while applying custom charges and re-rating pricing models – all based on flexible policy-based billing rules.

Granular visibility for better accountability

Billing Engine will provide at-a-glance views as well as customizable dashboards, charts, and reports on cloud costs, including cost customizations to give you the information you need the way you need it to support your business objectives. Data can be grouped by accounts and filtered/sorted for easy analysis by the enterprise, MSP, and MSP’s end customers (also known as L1/L2 relationships). With Billing Engine, you will be able to track costs and assess profits across all cloud providers at the macro level as well as drill down for more insights. These insights can help you determine the total cloud costs for specific products and/or services, identify cost overruns and assess profitable/unprofitable projects, and monitor progress with cost management initiatives and ROI to drive better budgeting and financial and business accountability.

Broad cloud provider support

Utilizing the FinOps Foundation’s FOCUS specification, Billing Engine supports AWS, Azure, and Google Cloud as well as SaaS provider billing data including Snowflake, Datadog, and others. Additional cloud providers will be supported in the future.

FOCUS: Committed to the open standard for cloud cost, usage, and billing data

Supporting the different and often conflicting billing formats used by the various cloud providers is challenging for both organizations and vendors. Individual names and identifiers as well as foundational concepts like cloud accounts can vary from provider to provider, making it difficult to analyze costs consistently across multi-cloud environments.

The FinOps Foundation’s FinOps Open Cost & Usage Specification (FOCUS) project is working to solve this challenge by developing an open specification that makes cloud billing data easier to understand for multiple cloud providers and vendor products. It aims to remove the complexity and overhead from common processes for cost allocation, chargeback, budgeting, forecasting, and other important processes.

As both a Premier member of the FinOps Foundation and a steering committee member of the FOCUS project, Spot is actively involved in developing this specification. Both Billing Engine and Cost Intelligence utilize version 0.5 of the FOCUS standard to ingest and normalize cost data from cloud providers. Through this support, these products can transform costs uniformly and ensure accountability consistently whichever cloud provider you are using. Our products will support the recently announced version 1.0 within the next few weeks.

Supporting customers throughout their FinOps journey

Over the next few months, we will be delivering many more exciting new capabilities as we further develop our FinOps offerings for both enterprises and MSPs. We are committed to empowering our customers not only to control and optimize their costs so that each dollar spent goes further than the last, but also to drive an efficient, optimized cloud environment that supports the customer experience and business growth.

Take the next steps

- Interested in a private preview? Request a demo today.

- Existing CloudCheckr customers who are interested in the new FinOps capabilities are encouraged to discuss their interest and strategy with their Technical Account Manager.